Questions Float about IPO ticket-clip -

The mooted litigation-funded class action against the Wynyard Group faces an immediate two-fold problem. This is exactly what entities are in the firing line of this proposed action, and how will any desired reparations be extracted from these entities?

Are we looking here, for example, at Britain’s Skipton Building Society? This financial services organisation is usually cited as controlling the Jade computer services organisation from which the Wynyard Group originated.

There are several problems here.One is that the Skipton Building Society–Jade organisation’s association with Wynyard Group is rather more tenuous than is widely supposed. For example, instead of seeding its new offspring with funding, the British organisation appropriated for itself a very large part of the original investment from the NZX flotation. The exact benefit of this to the fledgling offspring, the Wynyard Group and its shareholders has been complex to define and similarly with the labyrinthine ensuing cross-over obligations between the two companies.

If the Wynyard class action group has in its sights any other investors and/or promoters in Jade then there is the problem now of their being domiciled outside the Westminster jurisdiction. This especially applies to Jade investors in the United States.

In so many ways the Wynyard Group flotation represented New Zealand equities investors at their finest and most patriotic in their willingness to put their money behind the home team. You have to live in Christchurch to understand the intensity of this willingness to back the local side which Jade once was, and so, much more recently, was its Wynyard offshoot.

In the event Jade began in the desert, the Saudi Arabian one, where two New Zealand programmers were working as IT specialists for a Saudi distributor of United States earthmoving equipment. A problem in the 1970s that hit the engineering and construction equipment and stock holding business everywhere was the arrival of double digit inflation. The danger to engineering suppliers in this was selling parts and even full scale pieces of equipment at below their replacement cost.

It was now that the two programmers, with time on their hands, set out to solve this problem. They did so by devising a real time and online (ie instantaneous) system which meant that price increases from suppliers rippled out to all warehouse and outlet supply depots across the planet and as they occurred. This was a colossal breakthrough by any standard and became more so as the two programmers now proceeded to package it and market it

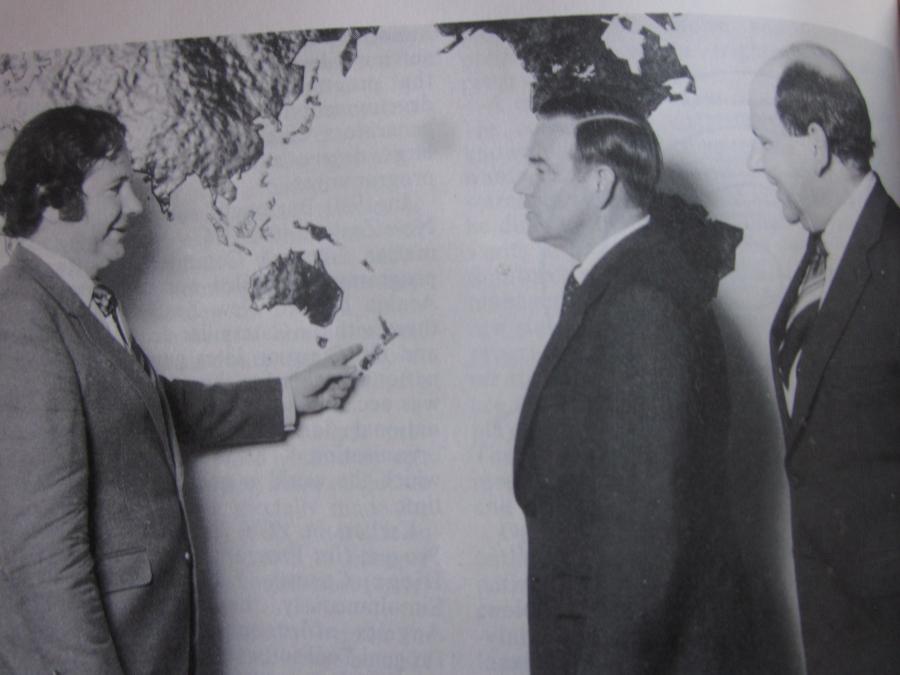

Burroughs, then a major force in world computing, ranking only just behind IBM, recognised the value of this discovery and in a remarkably short space time branded it as LINC (for logic and information network compiler) and put it in the very top shelf of their worldwide marketing. Our photograph shows Gil Simpson (at left) with his co-developer Peter Hoskin. In the middle is Robert Holmes the Burroughs top sider who oversaw the deal.

It was now that Jade made Christchurch in the 1980s one of the world hubs of network computing science. It really was a “centre of excellence.” The Linc compiler with its rapid implementation automated programming was the unique selling proposition, the secret. While the Linc project never actually became fourth generation (as was widely claimed for it) the product in that era got as close as any other system did to replicating the wave or multi-processing operation of the human brain.

All the rest followed. The Jade Stadium, Sir Gil Simpson Drive, and of course Sir Gil himself. Peter Hoskin, the co-developer, faded out of direct involvement and in recusing himself became the New Zealand version of those other early self-sidelined co-developers Paul Allen and Steve Wozniak.

Time moved on, and it was now that as so often in the IT sector, time from being an ally now manifested itself as a problem, especially at Burroughs, which by now had re-named itself Unisys. It was still a big-iron, mainframe manufacturer of centralised computers. It was now besieged by the personal computer manufacturers.

Even as Burroughs – Unisys became distracted, it was still able to use its muscle in its stronghold of mainframes to insert the Jade Linc system into the financial sector notably in the United Kingdom. It was now that started the supplier-client relationship of Jade with the Skipton Building Society.

Exactly why, and how Skipton became anchor investor in Jade remains largely unclear. There are though grounds for believing that Skipton needed to protect its own investment in its own Jade systems and did so by investing in the supporting supplier.

Even so, Jade was careful always to diversify its own market and took up a strong footprint in logistics, a natural growth sector deriving from its original inventory management expertise.

It was as part of this sector application diversification scheme that Jade sought out still newer fields in which to apply its compiler expertise. Law enforcement/risk management made sense.

Jade was by now encountering the problem of companies outside the United States to the effect that no matter how effective their products, no matter how much they tuned and re-tuned their underpinning quantum mechanics not to mention their marketing, they still seemed the poor relation to Silicon Valley. Especially in its ability to launch torrential new products on a marketplace that had become attuned, if not addicted to fast-rotating product issue frequency.

Canada’s Research in Motion with its Blackberry and Finland’s Nokia are two examples of seemingly invulnerable companies that succumbed to this kind of Silicon Valley rolling release.

Wynyard for example walked into this kind of Silicon Valley deep-pocket storm when it found itself confronted with sometime New Zealand resident and Tolkien buff Peter Thiel’s Palantir crime product.

Wynyard because of its Anglo-United States lineage had about it from the start an aura of the gilt edge. This halo was emphasised by its role as New Zealand’s first heavy-end departmental-capability IT main board listing. As is the IT custom everywhere the claims and forecasts made on its behalf contained a show-business extravagance and the executives seemed more photogenic than in other industries. The explanation for this multiplier is that if you win big in IT you win bigger than you do in other industries.

In the event, and as we can all see now, it was highly speculative and depended for its success on an early investment take up. One ideally in the form of a mainstream merger or acquisition that would have given Wynyard scale and the global distribution and sales and support channels that it always needed.

It does now all seems so unfair. Jade in its day took automated programming, meaning fast setup, further than any other technology outfit anywhere. It survived the 1987 bust, the dot com bubble, and the Great Financial Crisis.

But now its offshoot and which carries its pedigree is left to fade unfinished into the history of New Zealand ultra-advanced technology.

From the MSCNewsWire reporters' desk - Wednesday 2 November 2016